What Credit Score Do Mortgage Lenders Use

What’s my credit score? How do I make it better so that I can buy a house? When people have these questions, the internet gives the same typical responses. Go get a free version of your credit score. Sign up for a credit monitoring app. Then, follow the usual tips and tricks to raise your score.

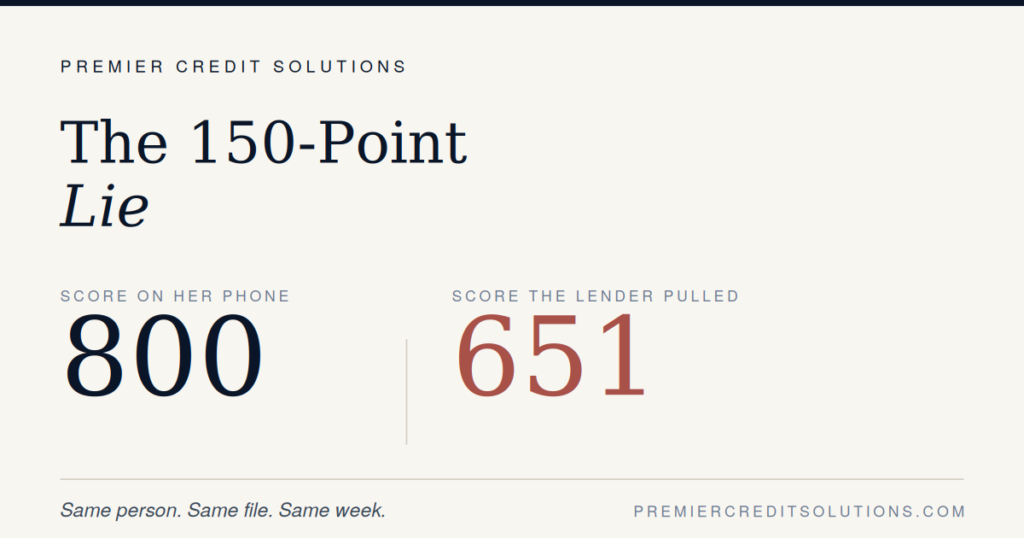

They watch their credit score rise on their credit card app or Credit Karma account. But when they go to the mortgage lender, they get a big surprise. Their credit score is lower than they thought — sometimes by 80 points or more.

This can be shocking, and it can derail your plans for homeownership. People in this situation are confused, and they have a lot of questions. What’s happening? Why don’t I have the right score? Why is the mortgage lender’s score different than the one Credit Karma gave me?

Here is the quick answer — there are many different types of credit scores. Mortgage lenders don’t use the same scores as credit card companies or credit tracking apps. They use a very specific FICO score.

If you have great credit, your score is going to be similar across the board, and you really don’t need to worry about the different types of credit scores. But if your score is in the poor, fair, or good range, you are going to see some differences, and they can hurt you when you go to apply for a mortgage.

You may not be able to get a mortgage at all, or you may end up incurring a higher interest rate. Even a percentage point can make a significant difference. On a $300,000 mortgage, going from a 4 to a 5% interest rate costs $167 a month and $64,000 over the life of a 30-year loan. The difference gets even more drastic with higher interest rates.

Credit Repair Services for Mortgage Applicants

This is when a lot of people call me. Typically, they say, “I’ve been trying to build my credit score. I thought it was increasing, but when I talked to the lender, it was a lot lower than I thought. What have I been doing wrong? Why is my score different than I thought?”

That’s when I explain the different types of credit scores. Then, we start talking about exactly what they need to do to improve their score to get a mortgage.

These clients boost their scores, take out mortgages, and buy great homes. But if I could change one thing about the process — I wouldn’t have them find out about the different types of credit scores when they’re in the mortgage lender’s office

By this time, they’ve already spent a lot of time trying to build their credit. They may have even already picked out their dream home. This is a frustrating point to realize that mortgage lenders use different scores.

But it doesn’t have to be this way. You can find out about the credit scores that mortgage lenders use before you apply for a loan. Then, you can work on improving that particular score, rather than wasting your time focusing on an irrelevant score.

What Are the Different Types of Credit Scores?

The main types of credit scores are FICO and VantageScores, and there are several different versions of each of these scores. Mortgage companies use the following scores:

- FICO Version 5 from Equifax (also called Equifax Beacon 5.0)

- FICO Version 2 from Experian (also called Experian/Fair Isaac Risk Model V2SM)

- FICO Version 4 from Transunion (also called TransUnion FICO Risk Score)

In contrast, Credit Karma uses VantageScore 3.0. Your credit card company probably uses the newest or second newest version of the FICO score — Right now, FICO is up to version 9. That means that mortgage lenders are using pretty old versions of FICO scores.

Which Credit Scores Do Mortgage Companies Use?

Which of the three credit scores do mortgage lenders use? Typically, they use the middle score, but if two of the scores are the same, they use that number regardless of whether it’s higher or lower than the other one. If the lender only has numbers from two credit reports, they take the lower one.

What Credit Score Do Mortgage Companies Use for Joint Applicants?

When two people want to get a mortgage together, the mortgage lender picks a score for each applicant based on the process explained above. Then, the lender uses the lower of the joint applicants’ scores.

Now that you know what credit scores mortgage companies use, you just have to find that number and get to work on improving it, right? That will certainly help. But it’s not that simple. There are a few other points you need to consider.

Do Mortgage Companies Only Look at Credit Scores?

Mortgage lenders also consider financial elements that don’t appear on your credit reports such as your income, time at your current employer, and your address history. The majority of mortgage loans issued in the United States must conform to Fannie Mae and Freddie Mac standards, and these government-backed companies have their own creditworthiness models and underwriting rules.

Most recently, Fannie Mae and Freddie Mac started paying attention to trended data. This highlights specific patterns with your credit card usage. In particular, it looks at whether you pay off your balance every month or let it roll to the next month. Mortgage lenders see people who carry balances on their credit cards as risky borrowers. They prefer to work with people who pay off the balances in full every month.

But most FICO scores don’t reflect these patterns. Instead, they put emphasis on credit utilization. As a result, someone who has a good or high score based on low utilization may have issues during the underwriting process when the trended data gets taken into account.

What if you’re looking for a non-conforming mortgage that doesn’t take Fannie Mae or Freddie Mac standards into account? Then, you’re probably going to be dealing with a bank’s custom scoring models for its jumbo mortgage products. You need to reach out to the lender to see what score they use and what other factors they consider.

Why Are There Different Types of Credit Scores?

There are different types of credit scores because lenders want to take different pieces of information into account when reviewing your creditworthiness. An auto loan lender wants to know whether or not you’re likely to repay an auto loan. A credit card company wants to know if you’re likely to repay a credit card. A mortgage lender wants to know that you can repay a mortgage.

Each of these different types of lenders uses a credit score that supports the specific goals of their transaction. The auto lender, for example, uses a credit score that puts more weight on your payment history and performance with past auto loans. Credit scores don’t exist for consumers. They exist so that borrowers can make judgments about consumers.

That’s why you need to know which credit score your mortgage lender is using. Then, you can engage specific tactics that help you increase that particular score.

How Can I Find the Credit Scores Mortgage Companies Use?

Unfortunately, you can’t get these scores for free. You have to pay for them, and you should go right to the source. FICO generates these scores, and you can get them on MyFICO.com.

The Advanced Monitoring Plan costs $29.95 per month. It gives you constant access to your FICO 8 score, and every quarter, it lets you see all of your scores. That includes all of the different versions of FICO scores that mortgage lenders use. At $39.95 per month, the Premier Monitoring Plan costs a little more, but it gives you access to all of your FICO scores on a monthly basis.

If you want to improve your credit score quickly so that you can buy a home, you need monthly updates to track your progress. If you’re working toward a longer-term goal, quarterly numbers can work just fine.

Don’t worry about this hurting your credit. It’s a soft pull. That means you get to see your score, but looking doesn’t hurt your score. In contrast, a hard pull is when a lender pulls your credit report because you’ve submitted a credit application. That can ding your score a little bit.

What Credit Scores Can You Get for Free?

But wait, you might be thinking, I thought I could get a credit score for free. I thought it was required by the law. Well, not exactly. Under the Fair and Accurate Credit Transactions Act (FACTA), each of the three major credit bureaus is required to provide you with a free credit report at least once a year, but those reports don’t include scores.

You can’t get the credit scores that mortgage companies use for free, but you can get all kinds of other scores for free. Here are the credit scores that different companies give out for free or when you sign up for their services:

- Transunion: VantageScore 3.0

- Equifax: VantageScore 3.0

- Experian: FICO 8

- Bank of America: FICO 8

- Wells Fargo: FICO 9

- Chase-Chase Journey: VantageScore 3.0

- Citibank: FICO Bankcard 8

- Discover: FICO 8

- Capital One-Credit Wise: VantageScore 3.0

- Credit Karma: VantageScore 3.0

- Credit Sesame: VantageScore 3.0

- Freecreditscore.com: FICO 8

- Nerdwallet: VantageScore 3.0

Why Do Mortgage Companies Use Old FICO Scores?

The reason that mortgage companies use FICO scores is that this was the first scoring model on the market. The first FICO score was generated in 1989, and Fannie Mae and Freddie Mac began using these scores in 1995.

The company that creates the FICO score is the Fair Issac Corporation. FICO stands for Fair Issac Co. It’s a data analytics company that was founded in 1956 by Bill Fair and Earl Isaac.

Currently, FICO has a 90% share in market applications. Lenders purchase billions of these scores every year, and millions of Americans access their own scores.

Upcoming Changes to Mortgage Credit Scores

In the next few years, mortgage lenders are planning to change the credit scores they use. In October 2022, the Federal Housing Finance Agency (FHFA) announced changes to the credit scores that Fannie Mae and Freddie Mac will use in the future. Rather than using the Classic FICO score that they have been using for almost 20 years, the agencies will transition to FICO 10T and VantageScore 4.0.

The change is designed to treat borrowers more fairly and to protect the security of the mortgage market. Both the FICO 10T and the VantageScore 4.0 include payment history on rent, utilities, and telecom payments when available. This stands to expand mortgage loan access to a wider range of people, making buying a home more equitable. Additionally, the enhanced accuracy of these scores should reduce risk for lenders.

On top of that, the FHFA also announced that lenders will only need to look at two credit reports rather than three. This is designed to reduce costs for lenders.

Unfortunately, the change will not happen immediately. The FHFA did not specify a timeline in its announcement, but it indicated that there will be a multi-year transition period. To put the timing into perspective, the FHFA started talking about making this change in 2014.

It’s important to note that Credit Karma currently uses VantageScore 3.0. When the mortgage industry transitions to using the new scores, Credit Karma will likely continue giving out the 3.0 score for free, but if you want to see VantageScore 4.0 used by the mortgage companies, you will almost certainly still have to pay for it.

What's the VantageScore Credit Score?

Created in 2006, VantageScore is a competitor of FICO, but the vast majority of its scores are used by credit card companies, not mortgage lenders. The VantageScore and the FICO score look at similar elements on your credit report. They both take into account outstanding debt, credit utilization, payment history, delinquencies, etc, and they both generally generate scores that fall in the 300 to 850 range.

However, these two companies use different methods to generate their scores. They also have different versions of their scores that rely on different algorithms.

The change is designed to treat borrowers more fairly and to protect the security of the mortgage market. Both the FICO 10T and the VantageScore 4.0 include payment history on rent, utilities, and telecom payments when available. This stands to expand mortgage loan access to a wider range of people, making buying a home more equitable. Additionally, the enhanced accuracy of these scores should reduce risk for lenders.

On top of that, the FHFA also announced that lenders will only need to look at two credit reports rather than three. This is designed to reduce costs for lenders.

Unfortunately, the change will not happen immediately. The FHFA did not specify a timeline in its announcement, but it indicated that there will be a multi-year transition period. To put the timing into perspective, the FHFA started talking about making this change in 2014.

It’s important to note that Credit Karma currently uses VantageScore 3.0. When the mortgage industry transitions to using the new scores, Credit Karma will likely continue giving out the 3.0 score for free, but if you want to see VantageScore 4.0 used by the mortgage companies, you will almost certainly still have to pay for it.

How to Improve Your Credit Score to Get a Mortgage

First of all, stop looking at credit scores that your lender doesn’t care about. Boosting your credit score takes hard work, but your efforts are wasted if you’re focusing on the wrong score. Find the credit score that your lender is going to use. Then, make a dedicated effort to improve that specific score.

To get started, give us a call. We’ll talk with you about your goals and look at your credit report with you. Then, we’ll help you customize a credit repair plan that boosts the scores your lenders are going to look at.

Don’t waste time with free credit score apps. Instead, get the information that you really need so that you can reach your goals. Ready to get started? Then, contact us today. We combine speed and skill so that most of our clients start seeing results in two to four weeks.

However, these two companies use different methods to generate their scores. They also have different versions of their scores that rely on different algorithms.