There’s a 150-point gap between your everyday credit score and your mortgage credit score — and most borrowers don’t find out until it’s too late.

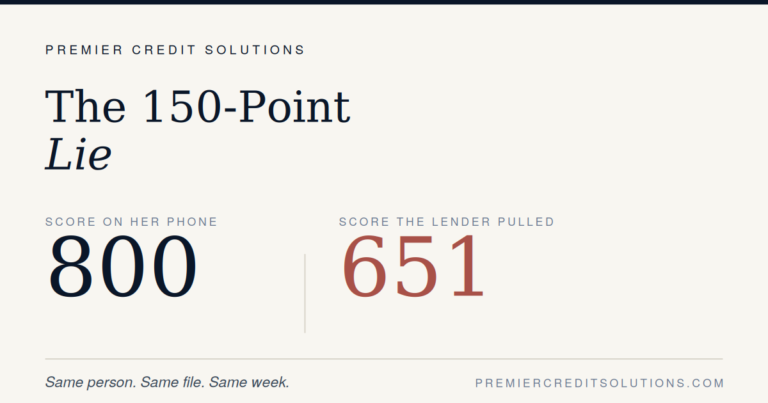

A borrower walks into the conversation with an 800 on her phone.

Credit Karma says 800. Her Chase app says 800. She’s been watching that number climb for two years. She’s done the work. She’s ready.

Then the lender pulls her actual mortgage credit score and the score comes back at 651.

That isn’t a mistake. That isn’t the lender being unfair. That’s the system working exactly the way it was designed to work. And nobody — not Chase, not Credit Karma, not the credit bureaus themselves — has any incentive to tell her the truth about it.

So I will.

Why your mortgage credit score isn’t the score on your phone

FICO doesn’t make one credit score. FICO makes a family of credit scores — different scoring models for different kinds of decisions. There’s a version for credit card decisions. There’s a version for auto loans. There’s a separate version for mortgages.

These are not the same number. They are not even the same calculation.

The mortgage version is the one that determines whether you get approved, what rate you get, and what the loan will cost you over the next 30 years. It’s also the version your credit card app will never show you. Not because anyone is hiding it. Because mortgage scores are a paid product. Lenders pay to access them. The free version you see in your phone is calibrated for a different decision entirely.

How big is the gap between the free version and the mortgage credit score version? I’ve seen it as wide as 150 points. App said 800. Mortgage pull came back at 650. Same person, same credit file, same week.

If your free score is telling you you’re ready, you might not be. If your free score is telling you you’re underwater, you might be fine. There’s only one way to know which side of that 150-point gap you’re actually standing on.

Spend $30. Save thousands.

Go to MyFico.com. Pay roughly $30 for one report. It provides the exact mortgage FICO score versions used in mortgage lending. If you pull MyFICO today and your lender pulls your mortgage scores today, the scores will match.

It doesn’t hurt your credit. And it’s the cheapest piece of pre-mortgage due diligence you will ever do.

The second lie: that fewer credit cards means better credit

Somewhere along the way, the financial advice industry decided that responsible credit means minimal credit. Pay off your cards. Close the ones you don’t use. Keep it lean. Stay disciplined.

FICO’s own data on the highest-scoring borrowers in America tells a different story.

FICO publishes research on what they call high achievers — the cohort of consumers with credit scores of 800 and above. The average 800+ profile has 11 revolving accounts. Six of those are traditional bank credit cards. Five are installment loans across their history. The oldest account on the file was opened 25 years ago. The newest account was opened, on average, more than two and a half years ago. Total utilization sits below 7%.

These are not people who panic-pay down their cards every month and close the ones they don’t use. These are people who opened the right accounts a long time ago, kept them, and barely use the limits they have.

Now compare that to the borrower with two credit cards and the conviction that two is enough. One late payment on a file that thin doesn’t get absorbed by the rest of the file. There is no rest of the file.

The floor for a resilient credit profile is somewhere in the four-to-six revolving account range. Not because the score rewards quantity. Because the score rewards depth, and depth requires accounts that have been open and active long enough to build a real track record.

What the scoring system cannot see

Credit scores are calculated from one thing: how you manage debt obligations.

That’s it.

The scoring system cannot see your income. It cannot see the balance in your savings account. You could have a million dollars in cash and the system has no mechanism to factor it in. You could have zero dollars to your name and a flawless 24-month payment history and the system will treat you as creditworthy.

The score isn’t built for that. It’s built to predict one thing — your probability of paying back a new credit obligation — based on a narrow set of inputs about how you’ve handled credit obligations in the past.

If you don’t have a track record, you don’t have a score. Your million dollars doesn’t fix that.

The trap that catches people after a credit setback

One trap I see after a major credit event — bankruptcy, divorce, medical, unemployment — is avoidance. People go through something painful, stop using credit entirely, and assume time alone will heal the file. It usually doesn’t. The damage stays visible while nothing healthy gets built around it.

There’s a second trap that catches people in the same situation: subprime credit card targeting. If you haven’t opted out of pre-screened mail offers, your mailbox starts filling up with credit card pitches. These offers are not accidental. They are aggressively targeted at damaged credit profiles — one of the most profitable segments in consumer banking. High interest rates, high annual fees, low credit limits. Eight or nine dollars a month in maintenance fees just to keep the card open. A $300 credit limit. An APR that would be illegal in some countries.

Those cards rarely rebuild credit the way borrowers expect. They keep the file looking subprime to future lenders, because that’s exactly what the file is — a subprime borrower with a subprime card, paying subprime fees.

What to do next

Three things, in order:

One — go to MyFico.com and pay for the real scores. You’ll know in 10 minutes whether you’re standing on the side of the 150-point gap you think you’re on.

Two — count your open, active revolving accounts. If the number is less than four, that’s not a moral failing, but it is a structural weakness in your file. Fixing it is straightforward and starts now, not the month before you apply for a mortgage.

Three — if there’s damage on your file you’ve been working around, stop working around it. Damage doesn’t age out faster because you ignore it.

If you want a second set of eyes on any of this from someone who reads credit files every day, that’s what Premier Credit Solutions does. After 25+ years inside lending decisions and more than 15,000 files analyzed, we’ll pull your real scores, walk you through what’s actually on the file, and tell you straight what’s realistic and what isn’t — before you spend earnest money on a property you might not be able to finance.

Book a free credit review at HERE.